What I Wish I Knew Before Losing My Job: Real Talk on Staying Afloat

Losing a job doesn’t just shake your income—it rattles your confidence, routine, and sense of control. I’ve been there, staring at bills with no paycheck coming. What saved me wasn’t luck, but a few practical money moves most people overlook. This is not about get-rich-quick schemes or soul-crushing budgeting. It’s about smart, doable strategies that protect your peace and your wallet when work disappears. The truth is, financial resilience isn’t built in crisis—it’s built before it. And while no one plans to lose their job, anyone can prepare to endure it with dignity, clarity, and a plan that holds.

The Moment Everything Changed

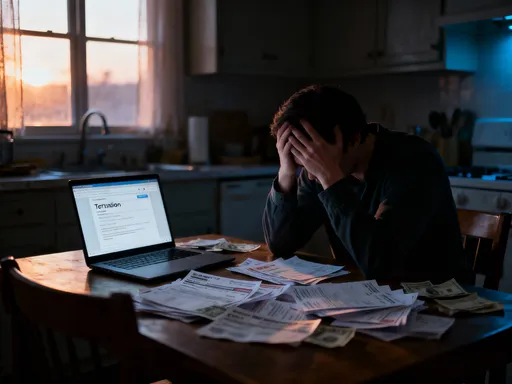

It happened on a Tuesday morning. A calendar invite titled “Check-in” turned into a five-minute conversation that changed everything. Just like that, the steady rhythm of biweekly paychecks, workplace routines, and future projections came to a halt. In the days that followed, the emotional toll was just as heavy as the financial one. There was disbelief, then anxiety, then a creeping sense of isolation. Even simple decisions—like whether to buy groceries or refill a prescription—felt loaded with risk. The stability I had counted on for years evaporated overnight.

What I didn’t realize at the time was that job loss is not just an economic event—it’s a full-scale disruption to identity and daily life. For many women in their 30s to 50s, especially those managing households or supporting families, the pressure multiplies quickly. You’re not just responsible for your own well-being; you’re holding together a network of dependents, schedules, and expectations. The fear isn’t only about money—it’s about failing to meet those responsibilities. Yet, what separates those who recover quickly from those who spiral isn’t income level or savings alone. It’s mindset. Those who treat job loss as a temporary setback, rather than a personal failure, are far more likely to take decisive action early.

That shift in thinking—seeing the situation as manageable, not catastrophic—was my first real breakthrough. I began asking different questions: What resources do I already have? What can I control? How long can I realistically stretch what I’ve saved? These weren’t magical solutions, but they grounded me. Instead of reacting emotionally, I started planning strategically. And in doing so, I discovered that preparation—both financial and psychological—can transform a crisis into a period of recalibration. The goal wasn’t to return to where I was, but to rebuild with greater awareness and strength.

Why Your Emergency Fund Isn’t Enough (And What to Do Instead)

Most financial advice says to keep three to six months of living expenses in an emergency fund. That guidance is sound in theory, but reality often exceeds expectations. When I lost my job, I had nearly five months of expenses saved. I thought I was safe. Yet within ten weeks, I had burned through nearly half that amount—not because I was reckless, but because unemployment brings hidden costs that aren’t part of your regular budget. COBRA premiums for health insurance added $500 a month. My car, which had been reliable for years, needed unexpected repairs. And because I was home more, utility bills rose. These weren’t luxuries—they were necessities that strained my cushion faster than I anticipated.

The flaw in the traditional emergency fund model is that it assumes income loss is the only variable. In truth, expenses often increase during unemployment due to medical coverage gaps, transportation for interviews, or even emotional spending triggered by stress. Relying solely on cash savings creates a false sense of security. A more resilient approach is what experts call a tiered emergency plan—a layered strategy that includes not just savings, but access to credit, liquid assets, and flexible living arrangements.

Start by calculating your true monthly burn rate during unemployment. Include insurance, minimum debt payments, groceries, utilities, and any job search costs like resume services or professional attire. Then, assess how long your cash reserves will last at that rate. Next, identify secondary resources: a low-interest credit line, a Roth IRA (where contributions can be withdrawn penalty-free), or even a side room you could rent temporarily. These aren’t defaults—they’re part of a thoughtful backup system. The idea isn’t to use them all at once, but to know they exist.

Another often-overlooked factor is geographic flexibility. If housing is your largest expense, consider whether relocating—temporarily or permanently—to a lower-cost area could extend your runway. This doesn’t mean drastic moves, but exploring options like staying with family for a few months or negotiating a lease pause can buy critical time. The goal is to create multiple layers of protection so that if one fails, others remain. Financial resilience isn’t about having everything in cash—it’s about having options.

Cutting Costs Without Killing Your Spirit

When income stops, every dollar takes on new meaning. But cutting back doesn’t have to mean sacrificing dignity or joy. The key is distinguishing between essential needs and discretionary spending—and doing so without shame. I started by reviewing every bill and subscription. The streaming services I barely used? Paused. The premium grocery delivery fee? Switched to in-store pickup. The gym membership I hadn’t visited in months? Canceled. These weren’t painful decisions—they were liberating. Each cut was a reclaiming of control.

Yet, the real danger isn’t in big expenses—it’s in the small, recurring leaks. A $15 app subscription here, a $4 daily coffee there—they add up quickly when income is gone. I tracked every expense for two weeks and was shocked to find I was spending over $200 a month on items I didn’t truly need. Once I saw the pattern, I could make intentional choices. I switched to generic brands, used coupons strategically, and planned meals around sales. These aren’t signs of hardship—they’re signs of wisdom.

More importantly, I refused to let frugality erode my mental health. I kept one small pleasure each week—a library book, a walk in the park, a phone call with a friend. These weren’t expenses; they were investments in emotional stability. The psychology of spending under stress is powerful. Anxiety can lead to overspending as a form of comfort, or underspending to the point of isolation. Balance is essential. You don’t need to live like a monk to be responsible. You need to live like someone who values both security and self-respect.

Another effective strategy was renegotiating fixed costs. I called my internet provider and asked for a retention discount. I reviewed my cell phone plan and downgraded to a cheaper tier. Many companies are willing to work with customers facing hardship, especially if you ask. The act of negotiating isn’t begging—it’s advocating for yourself. And every dollar saved this way extends your financial runway without requiring lifestyle sacrifice. The goal isn’t deprivation. It’s alignment—ensuring your spending reflects your current reality, not past habits.

Making Your Money Work While You Wait for Work

When your income stops, the last thing you should do is chase high returns. Desperation can lead to risky decisions—investing in speculative stocks, joining questionable “opportunity” programs, or pulling money from retirement accounts. I’ve seen people lose their entire savings this way, all in the hope of a quick fix. The truth is, during unemployment, your primary financial goal isn’t growth—it’s preservation. Your savings are not an investment portfolio right now; they’re a lifeline.

That doesn’t mean your money should sit idle. Even in a low-interest environment, there are safe ways to earn modest returns without taking on risk. High-yield savings accounts, for example, offer better interest than traditional banks and are FDIC-insured, meaning your money is protected. Short-term certificates of deposit (CDs) can also provide slightly higher yields with minimal risk, especially if you ladder them to maintain access to funds over time. These aren’t get-rich-quick tools, but they do help offset inflation and keep your savings productive.

The mindset shift here is crucial. Instead of asking, “How can I make money fast?” ask, “How can I protect what I have?” This changes everything. It removes the pressure to take reckless chances. It reinforces discipline. And it keeps your focus on the real objective: bridging the gap until your next income source begins. Remember, a 5% loss hurts far more than a 2% gain helps. Protecting capital is always the priority when income is uncertain.

Another important consideration is liquidity. Your money needs to be accessible when you need it. That means avoiding long-term investments or locked accounts unless you’re certain you won’t need the funds. It also means keeping emergency cash separate from other accounts to prevent accidental spending. I set up a dedicated account for essential expenses and transferred only what I needed each month. This created a psychological and practical barrier that helped me stay on track. In times of uncertainty, simplicity and safety outperform complexity and speculation every time.

Navigating Benefits and Hidden Support Systems

One of the biggest mistakes people make after job loss is delaying or avoiding benefits out of pride or confusion. I did it too. I waited three weeks to file for unemployment because I thought I should “figure things out first.” That delay cost me nearly $1,200 in missed payments. Unemployment insurance isn’t charity—it’s a benefit you’ve paid into through payroll taxes. Filing promptly ensures you receive what you’re entitled to without unnecessary gaps.

Beyond unemployment, there are other often-overlooked resources. COBRA allows you to continue your employer’s health coverage, but it’s expensive. Instead, I explored options through the Health Insurance Marketplace, where I qualified for a subsidy due to my reduced income. The monthly premium was less than half of COBRA’s cost. I also looked into local community health clinics, which offer low-cost care for routine needs. These aren’t fallbacks—they’re smart financial choices.

Many employers also provide outplacement services—career coaching, resume reviews, interview training—at no cost to departing employees. I used mine to refine my job search strategy and gained confidence I didn’t realize I’d lost. Some communities offer retraining programs or job fairs specifically for displaced workers. Libraries often host free workshops on digital skills or financial planning. These resources aren’t always advertised, but they exist. The key is to seek them out proactively, not wait to be told.

There’s no shame in using support systems. In fact, it’s a sign of strength. It shows you’re managing risk intelligently, not just surviving emotionally. Every dollar you save through benefits is a dollar that stays in your emergency fund. Every service you access reduces the burden on your personal finances. Think of these tools as part of your financial toolkit—not as handouts, but as strategic assets in your recovery plan.

Protecting Your Credit—Your Financial Lifeline

Credit is one of the most powerful yet fragile financial tools. During unemployment, it can either be a safety net or a trap. I learned this the hard way when I made a minimum payment late on a credit card—just one month. It didn’t seem like a big deal at the time, but it triggered a penalty fee and a rate increase. More importantly, it dinged my credit score. What I didn’t realize was that credit health affects far more than loan approvals. It influences rental applications, insurance rates, and even some job screenings.

The biggest threats to credit during job loss are missed payments and high utilization. When income stops, people often rely more on credit cards, pushing balances closer to their limits. Even if you make minimum payments, a high utilization ratio can lower your score. The solution isn’t to avoid credit altogether, but to manage it proactively. As soon as I knew my income would stop, I contacted my lenders. I explained my situation and asked about hardship programs. Many creditors offer temporary payment deferrals, reduced interest rates, or modified payment plans. These aren’t automatic—you have to ask.

I also made a rule: never use credit for non-essentials. My cards were reserved for groceries, utilities, and job search costs—nothing more. I set up alerts for due dates and scheduled payments as soon as I received unemployment funds. I also checked my credit report regularly through free services to ensure accuracy. One error I caught early—a duplicate account listing—could have damaged my score if left uncorrected.

Maintaining credit health isn’t about perfection. It’s about consistency and communication. A single late payment doesn’t ruin your future, but a pattern of missed payments can. By staying proactive, you preserve your financial reputation and keep doors open for the next chapter. When you’re ready to rent a new apartment or finance a car, your credit will reflect not the crisis, but how you managed it.

Building a Bridge, Not Just Surviving the Gap

Unemployment doesn’t have to be a detour—it can be a bridge. The difference lies in how you use the time. If you’re only focused on survival, you may take the first job offer out of desperation, even if it’s underpaid or misaligned with your goals. But if you create a financial bridge plan—a structured approach that aligns money management with your job search—you gain the space to make better decisions.

I defined my bridge by setting clear phases: stabilization (first 30 days), skill-building (next 60 days), and re-entry (90+ days). Each phase had financial and professional goals. In stabilization, I secured benefits, cut non-essentials, and protected credit. In skill-building, I used free online courses to update my resume and learned new software relevant to my field. In re-entry, I budgeted for networking events and professional photos. This structure gave me purpose and prevented aimless drifting.

Financial stability creates mental clarity. When you’re not constantly worried about the next bill, you can focus on long-term growth. You can negotiate better salaries, pursue meaningful roles, and avoid settling out of fear. My time without work became a period of reinvention, not just recovery. I emerged with a stronger resume, a clearer sense of direction, and a more resilient financial foundation.

The truth is, job loss is not the end of your story. It’s a chapter—one that can teach you more about strength, resourcefulness, and planning than any promotion ever could. The strategies that help you survive aren’t temporary fixes. They’re lifelong skills. By preparing in advance, cutting costs with dignity, protecting your credit, and using every resource available, you don’t just stay afloat. You build a foundation that carries you forward, no matter what comes next.